Tax Planning

Tax Planning For Ultra-High-Net-Worth Individuals The Average Person Earning $500K+

Overpays The IRS $52,000 Every Year.

Not because of bad intentions — because filing taxes and planning taxes are two entirely different things. At your income level, the gap between what you owe and what you're paying is likely the most expensive inefficiency in your financial life.

At $500K+ income, every year without a proactive tax strategy isn't just an oversight — it's a six-figure mistake. The IRS counts on you not noticing.

$52,000

avg. annual tax overpayment for individuals earning $500K+*

73%

of UHNW individuals have no coordinated, multi-strategy tax plan

37%+

combined federal rate hitting every dollar of unplanned ordinary income

$500K

minimum threshold where cost segregation, QSBS, and advanced strategies unlock

* $52,000 figure reflects estimated annual tax overpayment for $500K+ earners based on analysis by the Tax Foundation and studies by Vanguard and McKinsey on the value of financial advice, incorporating missed strategies including Roth conversions, tax-loss harvesting, charitable giving vehicles, and business income structuring. Individual results vary by income composition, deductions, and existing planning.

The UHNW Overpayment Audit Where ultra-high earners lose money every single year

These aren't obscure loopholes. They're strategies your advisor and CPA should already be doing — and in most cases, aren't.

| Missed Strategy | Typical Annual Loss | With Planning | Status |

|---|---|---|---|

Cost SegregationAccelerates depreciation on real estate by reclassifying components — turning a 39-year deduction into a 5–7 year one, generating massive near-term tax deferrals | −$50,000–$250,000+ | Deferred or eliminated | Rarely Used |

Roth Conversion StrategyConverting pre-tax retirement assets in strategic low-income years to permanently tax-free Roth accounts — eliminating a future tax liability that compounds for decades | −$40,000–$120,000+ | Long-term savings | Commonly Missed |

Tax-Loss HarvestingSystematically capturing portfolio losses to offset capital gains — at $2M+ in investments, this is an annual six-figure opportunity most advisors run manually, if at all | −$20,000–$60,000 | Annual recurring savings | Underexecuted |

Charitable Giving VehiclesDonor-advised funds and charitable remainder trusts using appreciated assets — far more effective than cash donations, yet most UHNW donors are still writing checks | −$15,000–$50,000 | Compounded deduction value | Commonly Missed |

Business Income Structuring (QBI + DBP)Qualified Business Income deductions, defined benefit plans, and entity structure optimization — business owners at this level have access to strategies that can shelter $100K+ annually | −$50,000–$150,000 | Recurring shelter | Often Underused |

RMD & Withdrawal SequencingRequired Minimum Distributions without a plan spike income into the top bracket — every year, permanently. A sequencing strategy built years in advance can eliminate this entirely | −$25,000–$80,000 | Lifetime bracket control | Rarely Planned |

Combined Annual Potential — $500K+ EarnerIllustrative composite across all strategies. Actual impact depends on income sources, asset base, and existing planning | −$200K–$700K+ | Recoverable | With a Plan |

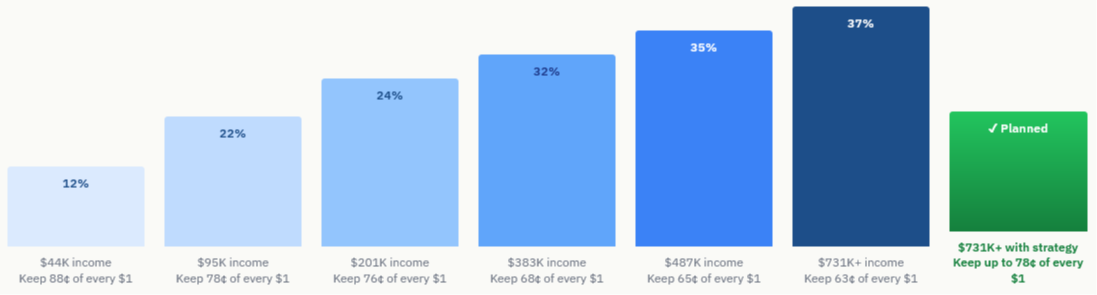

The Bracket Reality for High EarnersAt $500K+, you're in the top bracket — but strategy determines how long you stay there

The 37% federal rate is the floor for unplanned income at your level. UHNW tax planning is about legally reducing the amount of income that reaches that bracket — year after year.

★ The "Planned" bar reflects an illustrative estimate for a $731K+ earner deploying a coordinated UHNW strategy: cost segregation on real estate holdings, a defined benefit plan, Roth conversions in lower-income years, charitable giving through a donor-advised fund, and tax-loss harvesting across a $2M+ portfolio. Combined, these strategies can reduce the effective rate on a portion of income from 37% to the capital gains range or below. Individual results vary materially. Schedule a private consultation for your specific analysis.

UHNW Tax StrategiesThe strategies available at your income level — used or not

These aren't available to everyone. At $500K+ income or $1M+ in assets, you have access to a tier of tax strategy most people never see. Most don't use it because no one showed them it existed.

🏗️

Cost Segregation

If you own real estate — commercial or residential rental — cost segregation is one of the most powerful legal tax tools available. By reclassifying building components from a 39-year depreciation schedule to 5, 7, or 15 years, you dramatically accelerate deductions into the current year. A $1M property can generate $100K–$200K in year-one deductions that would otherwise be spread over nearly four decades.

Avg. impact: $50K–$250K+ in near-term tax deferrals per property

🔄

Multi-Year Roth Conversion Ladder

We identify windows — business sale years, market downturns, income dips — to convert pre-tax retirement assets to Roth at the lowest possible rate. At your asset level, this is a six- to seven-figure lifetime tax decision. Most advisors treat it as a one-time event. We treat it as a multi-decade strategy.

Avg. impact: $40K–$120K+ in long-term tax elimination

📉

Systematic Tax-Loss Harvesting

With $1M+ in investable assets, tax-loss harvesting isn't a minor courtesy — it's an annual six-figure opportunity. We build a systematic process that captures losses across your portfolio to offset realized gains, without disrupting your investment strategy or triggering wash-sale violations.

Avg. impact: $20K–$60K annually at $1M+ portfolio size

💝

Charitable Giving Architecture

Donor-advised funds, charitable remainder trusts, and private foundations — used together with appreciated assets — can dramatically increase the impact of your giving while generating immediate deductions and eliminating capital gains. If you're writing checks to charity, you're leaving money on the table.

Avg. impact: $15K–$80K annually depending on giving level

🏢

Business Income Structuring

Defined benefit plans can shelter $200K+ annually for business owners and the self-employed. Combined with QBI deductions, entity structuring, and deferred compensation plans, a coordinated business tax strategy can reduce your effective rate by 10–15 percentage points on operating income.

Avg. impact: $50K–$200K annually for business owners

📊

RMD Neutralization Strategy

Required Minimum Distributions without a plan force you into the top bracket — every year for the rest of your life. We build a multi-decade strategy to systematically reduce the pre-tax balance subject to RMDs, so when they arrive, they don't control your tax life.

Avg. impact: $25K–$100K annually in bracket management

The Real DifferenceSame $2M income. A very different tax bill.

This is what a $1,000,000 household income looks like with and without a coordinated UHNW tax strategy in place.

❌ Without UHNW Tax Planning

- No cost segregation — real estate depreciation spread over 39 years instead of accelerated

- No Roth strategy — all retirement assets remain in pre-tax accounts compounding a future tax liability

- Donations by check — no donor-advised fund, no appreciated stock gifting, no deduction optimization

- No defined benefit plan — business income fully exposed at 37% ordinary rates

- Portfolio gains unmanaged — short-term gains taxed at top ordinary rate, no harvesting offset

- No RMD strategy — deferred tax liability growing unchecked for decades

Estimated Annual Tax Bill

$368,000

✓ With HWMG UHNW Tax Strategy

- Cost segregation on two investment properties — $180K in accelerated first-year deductions

- Roth conversion executed in strategic window — $150K converted at reduced effective rate

- $75K charitable contribution via donor-advised fund using appreciated stock — full deduction, no capital gains

- Defined benefit plan funded at $220K — sheltered from ordinary income tax entirely

- Tax-loss harvesting offsets $85K in realized gains — capital gains bill cut significantly

- Multi-year RMD reduction strategy initiated — pre-tax balance shrinking on schedule

Estimated Annual Tax Bill

$204,000

Annual tax savings with coordinated UHNW strategy: $164,000

Illustrative example based on common UHNW strategies. Individual results vary materially based on income composition, asset base, real estate holdings, and existing planning. This is not tax advice — consult a qualified advisor for your specific situation.

Your CPA files your taxes.

We engineer them.

We offer a private, complimentary tax strategy review for individuals earning $500K+ or holding $1M+ in investable assets. We'll identify your specific overpayment, walk through every applicable strategy, and show you what a coordinated plan looks like for your situation.

Reserved for individuals earning $500K+ annually or with $1M+ in investable assets